Most conversations about reopening and frontier markets start from the same assumption: capital and expertise move in one direction. International organisations look outward, assess a market's readiness, and decide whether and how to enter. It is a natural starting point, and most readiness literature is written from that vantage point.

But it is an incomplete picture, and the parts it leaves out are not minor.

Reopening and structurally transitioning markets are not simply destinations waiting to be entered. They are also economies whose own companies and institutions need to engage outward — to access international partnerships, meet governance and compliance standards, raise capital beyond domestic sources, and participate credibly in cross-border trade. Treating this as a secondary concern, something that happens later or belongs to a different set of actors, misses how these markets actually develop — and weakens the inbound case as well.

The stronger framing is corridor thinking: reopening markets should be understood as two-directional corridors, not one-way doors.

The one-way assumption

The one-way view is intuitive because it mirrors how opportunity usually becomes visible. International organisations notice a market changing, assess whether conditions support engagement, and frame their strategic question as “how do we enter.” It is a legitimate question — but only half of one.

That question is not wrong. But the half that goes unasked — how ready the domestic side is to meet it — is usually more consequential than it first appears.

A reopening market's investability is not determined solely by regulation, institutions and macro conditions. It is also determined by the quality and international readiness of the domestic companies and institutions any inbound investor, partner or advisor will eventually work with. A market can be regulatorily open and still difficult to engage with, because the domestic side of the relationship has not yet built the governance, compliance and operating capacity cross-border engagement requires.

This is the same counterparty question that already shapes inbound readiness — simply viewed from the other direction.

What corridor thinking actually means

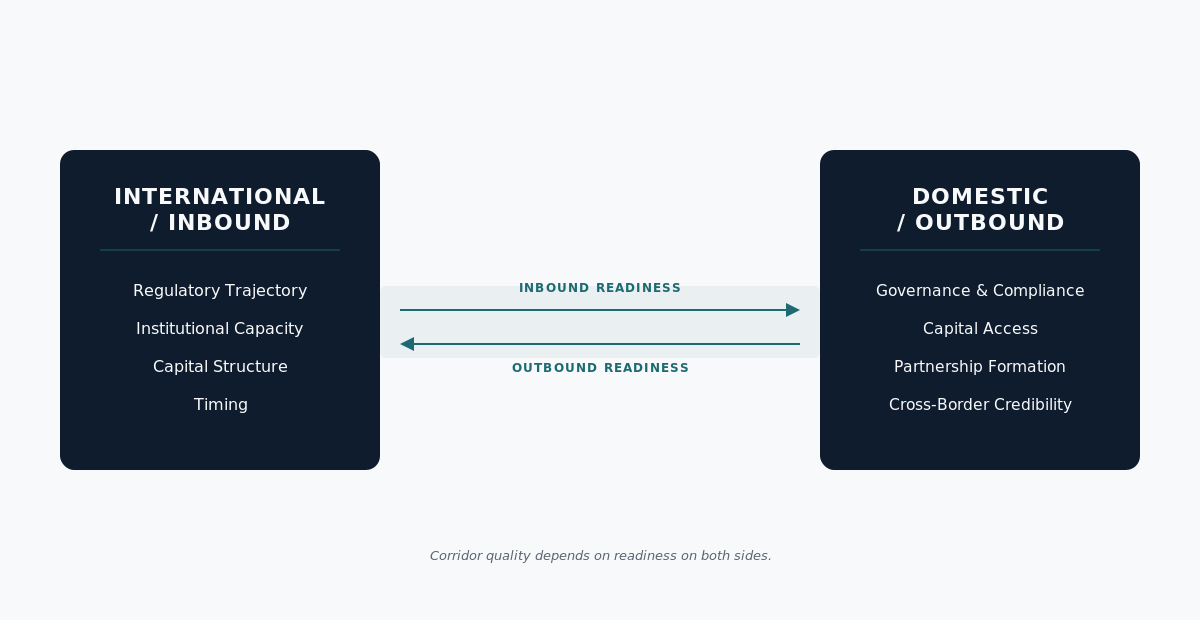

Corridor thinking treats reopening-market engagement as a two-sided structure rather than a single directional flow.

On one side sits inbound readiness: understanding a market's regulatory trajectory, institutional capacity, capital structure and timing — the conditions that determine whether an international organisation can engage responsibly, and when.

On the other side sits outbound readiness: preparing domestic companies and institutions to internationalise — to meet the governance, compliance and partnership standards cross-border engagement requires, and to become credible counterparties rather than passive recipients of external interest.

A corridor is not two separate markets — it is a single system, and the quality of engagement across it depends on the readiness of both sides. An inbound investor evaluating a reopening market is, in practice, also evaluating the outbound readiness of the domestic firms it will partner with, acquire, or compete against. The two cannot be fully separated, even though most strategic frameworks treat them as if they can.

Why the two sides are connected, not sequential

A common instinct is to sequence this: the market opens, international engagement builds confidence and capital, and only later — once the market has matured — do domestic firms develop the capacity to internationalise in return.

This sequencing is usually wrong, or at least unnecessarily slow. Domestic and inbound readiness develop in parallel, not in series, and reinforce each other when they do. A company that has already built governance discipline, financial transparency and partnership-readiness before international attention arrives is a stronger counterparty the moment it does — and a plausible outbound actor in its own right, rather than purely an object of inbound interest.

This matters strategically, because organisations that understand both sides of a corridor are positioned differently from those that understand only one. An investor or advisor focused solely on inbound entry sees a narrower opportunity set and a shallower view of counterparty risk. One that also understands what outbound readiness requires sees a fuller picture of where value and risk actually sit — and is positioned to engage earlier and more credibly on both sides of the relationship.

What outbound readiness actually requires

Outbound readiness is not a single capability. Like inbound readiness, it is a set of interacting conditions.

Governance and compliance maturity is usually the first constraint. International partners and capital providers evaluate counterparties against standards not yet standard practice domestically — financial reporting quality, board and ownership transparency, anti-corruption controls, and data and operational governance. Firms without these capabilities are difficult to engage with, regardless of how attractive the underlying business is.

Capital access is a second constraint. Domestic firms often have real growth potential but limited access to the kind of structured, patient capital — comfortable with cross-border complexity — that would let them scale beyond their domestic market. What kinds of capital are realistically available to them, and what those providers require in return, matters as much as capital availability from the inbound side.

Partnership formation is a third. Firms seeking to internationalise need to identify credible international partners, understand what those partners require, and structure engagement that survives due diligence — the mirror image of the counterparty work inbound investors already do, applied in the other direction.

Cross-border credibility is the cumulative result of the first three — not a marketing exercise, but the accumulated evidence that allows a domestic firm to be taken seriously by international counterparts without requiring unusual trust or risk tolerance from them.

What this means for organisations engaging with reopening markets

For investors, advisors and development-focused institutions working around reopening and frontier markets, corridor thinking changes the practical question — from “how do we assess this market for entry” to “how ready is the corridor, in both directions, for engagement to succeed.”

It is a more demanding question, and a more useful one. It surfaces what a purely inbound lens misses: domestic firms worth engaging before they are widely visible internationally, capital gaps a well-structured relationship could address, and governance support that improves a market's overall investability rather than just one transaction's outcome.

It also produces a more durable form of positioning. Organisations that only ever appear as inbound actors compete with every other inbound actor for the same visible opportunities. Those that understand the corridor as a whole occupy a less crowded, more defensible position.

The Raviston view

Reopening and frontier markets are not one-way opportunities waiting for outside capital to arrive. They are corridors, and corridors work in both directions at once. The domestic companies and institutions inside them are not simply the backdrop to inbound investment decisions — they are active participants whose own readiness to internationalise shapes what inbound engagement is actually possible.

Organisations that treat reopening markets as one-way doors keep competing for the same narrow set of visible opportunities. Organisations that understand the corridor — both what makes external engagement credible, and what makes domestic firms genuinely internationalisation-ready — are working from a fuller, more accurate picture of how these markets actually develop.

That fuller picture is not a niche concern. It is the difference between assessing a market and understanding it.

About Raviston

Raviston is a threshold intelligence and strategic advisory firm focused on frontier, reopening and structurally transitioning markets. Raviston helps organisations understand both sides of market transition — the conditions that make inbound engagement credible, and the readiness domestic firms need to internationalise, access capital, and position for cross-border growth.